ProduceIQ: Markets cool as holiday supply takes shape

Week #50 index prices are down 10 percent over the previous week as production of heavily weighted commodities ramped up.

Images courtesy ProduceIQ

’Twas the week before Christmas, and across the country, produce prices are on the decline.

Week #50 index prices are down 10 percent over the previous week as production of heavily weighted commodities ramped up across both Western and Eastern growing regions.

Much like the stocking hung by the chimney with care, supply is finally falling into place, bringing a welcome reset to markets that have spent much of the season elevated.

ProduceIQ Index: $1.09/pound, -10.0 percent over prior week

Week #50, ending Dec 12th

Blue Book has teamed with ProduceIQ BB #:368175 to bring the ProduceIQ Index to its readers. The index provides a produce industry price benchmark using 40 top commodities to provide data for decision making.

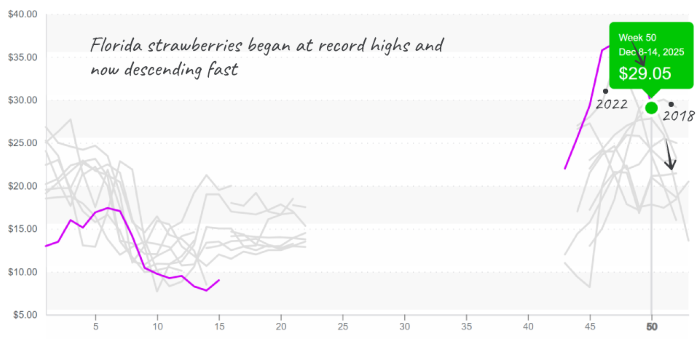

Strawberry markets are showing clear signs of recovery. In line with last week’s forecast, average prices declined 33 percent week over week, settling at $29. While this level narrowly avoids record-breaking territory, markets remain well above the historical average for Week #50.

Although West Coast producers continue to report volumes on the lower end of the historical range, rapidly increasing supplies from Florida are creating early opportunities for deals on large-volume orders.

Florida strawberries have increasing supplies, causing prices to plummet from record highs

While berries move lower, not all commodities are following the same script, a reminder that even as visions of sugar-plums fade, certain items continue to defy gravity. Brussels sprouts continue to show strong upward momentum, standing out sharply from the broader market pullback. Average prices have reached a ten-year high by a wide margin. Moisture-related quality issues, including insect pressure, decay, and shortened shelf life, are affecting available supplies. Production from Mexico is slowly increasing but is unlikely to adequately meet demand until January.

Celery markets remain similarly constrained, reinforcing the theme of selective strength amid otherwise easing conditions as the holiday pull peaks. Prices are at their second-highest level in the past ten years as supplies out of Oxnard increase only gradually and Salinas growers near the end of their season. Strong holiday demand combined with limited production is expected to keep prices elevated through Christmas.

Celery supplies continue to struggle, allowing prices to test the highs of 2022 [accidentally wrote 2023 in the graph]

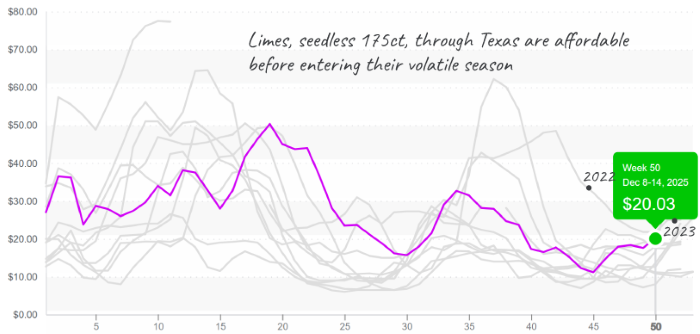

As the calendar winds down and buyers make their final lists, citrus markets reflect typical end-of-year patterns. In line with seasonal trends, lime prices are on the rise, up 15 percent over the previous week, with potential for further acceleration into January. Unlike prior years, markets are starting from a higher baseline due to sizing constraints. The old crop is nearly finished, while the new crop is just beginning.

As demand surges and availability shifts, some vulnerability should be expected. Holiday demand and sizing fluctuations over the next three weeks are likely to keep lime markets active and unpredictable as the year draws to a close.

Lime prices are as expected for this time of year; volatility typically begins after January

ProduceIQ saves you time and provides valuable information to increase your profits.

The ProduceIQ Index is the fresh produce industry’s only shipping point price index. It represents the industry-wide price per pound at the location of packing for domestic produce and at the port of U.S. entry for imported produce.

ProduceIQ uses 40 top commodities to represent the industry. The Index weights each commodity dynamically, by season, as a function of the weekly 5-year rolling average Sales. Sales are calculated using the USDA’s Agricultural Marketing Service for movement and price data. The Index serves as a fair benchmark for industry price performance.

News you need.

Join Blue Book today!

Get access to all the news and analysis you need to make the right decision --- delivered to your inbox.

Subscribe to our newsletter

© 2026 Blue Book Services. All Rights Reserved